Exploring Ugod Net Worth: What Really Shapes Financial Standing?

Have you ever wondered about someone's financial picture, maybe thinking about their overall wealth? It's a common curiosity, and when the phrase "ugod net worth" pops up, it naturally sparks questions about what that really means. A person's net worth, you see, is a snapshot of their financial health at a particular moment. It's essentially what you own minus what you owe, a simple idea that, when you get down to it, involves quite a few moving parts. For a name like "ugod," which isn't widely known from the information we have, we'll look at the general principles that help us figure out how someone's wealth is measured. So, how do we even begin to figure out such a thing?

When people talk about someone's net worth, they're often trying to get a sense of their accumulated assets, like property, investments, or even valuable possessions, weighed against their debts, such as loans or mortgages. It's not just about how much money someone makes in a year, which is income, but rather the total value of everything they possess once their financial obligations are taken away. This can be a bit more involved than it sounds, as there are many different things that can contribute to or detract from this figure. In a way, it’s like taking a full inventory of a person's financial life.

Understanding "ugod net worth," then, becomes an exercise in looking at the general factors that build wealth for anyone. Since the provided text doesn't offer specific details about "ugod" or their financial background, we'll explore the common elements that contribute to a person's financial standing. This means we'll be thinking about income streams, various types of investments, and even the role of debt. It's a rather broad topic, but it helps us grasp the concept, you know, even without a specific person in mind. We'll talk about how these pieces fit together to form that overall financial picture, and why it matters.

Table of Contents

- What Exactly is Net Worth?

- Key Components of Net Worth: Assets and Liabilities

- Common Ways People Build Wealth

- Factors That Can Influence Net Worth

- How Net Worth is Often Estimated (Without Specific Data)

- Tips for Building Your Own Financial Strength

- People Often Ask

What Exactly is Net Worth?

Net worth, at its core, is a simple calculation: it's the total value of all your assets minus all your liabilities. Think of assets as everything you own that has monetary value. This could be cash in the bank, money in investment accounts, real estate, vehicles, or even valuable collectibles. Liabilities, on the other hand, are all your debts or financial obligations. This includes things like mortgages, car loans, credit card balances, student loans, and any other money you owe. So, really, it's a straightforward equation, but the items within it can be quite varied.

When someone talks about "ugod net worth," they're referring to this exact calculation for that particular individual or entity. A positive net worth means you own more than you owe, which is usually a good sign of financial health. A negative net worth means your debts are greater than your assets, which suggests a need for careful financial planning. It’s a bit like a financial report card, showing where you stand. This figure changes constantly, too, as asset values go up and down, and debts are paid off or taken on. It’s a dynamic measure, to be sure.

It's important to remember that net worth isn't the same as income. Income is the money you earn over a period, like a salary or business profits. Net worth is a cumulative measure, reflecting all the wealth you've built up over time. You could have a high income but a low net worth if you spend a lot or have significant debt. Conversely, someone with a modest income might have a substantial net worth if they've been good at saving and investing for a long time. So, they're distinct concepts, though they are related, as income often helps build net worth, you know.

Key Components of Net Worth: Assets and Liabilities

To truly grasp "ugod net worth," or anyone's financial standing for that matter, we need to break down the two main parts: assets and liabilities. Assets are things that put money in your pocket or could be turned into cash. They come in many forms, and understanding them is key to seeing the full picture. You've got your liquid assets, which are things easily converted to cash, like savings accounts or checking accounts. Then there are investment assets, which include stocks, bonds, mutual funds, and retirement accounts. These often grow over time, which is pretty neat.

Assets: What You Own

Cash and Equivalents: This is the most straightforward asset. It includes money in checking accounts, savings accounts, and money market accounts. It's readily available, so it's a very liquid asset, you see.

Investments: This category is usually a big one for building wealth. It covers stocks, bonds, mutual funds, exchange-traded funds (ETFs), and even alternative investments like private equity or hedge funds. Retirement accounts, such as 401(k)s, IRAs, or pensions, also fit here. These are designed to grow over the long haul, which is often the plan.

Real Estate: For many, their home is their biggest asset. This also includes any other properties owned, like rental properties, vacation homes, or land. The value of these properties contributes significantly to net worth, so it does.

Personal Property: This includes valuable items like vehicles, jewelry, art collections, or other tangible possessions that have a resale value. While not always easy to liquidate quickly, they still add to the overall asset total, you know.

Business Interests: If "ugod" owned a business, the value of that business, or their share in it, would be a major asset. This could be a small local shop or a large corporation. The value of a business can be quite substantial, actually.

Liabilities: What You Owe

On the flip side, liabilities are the debts that reduce your net worth. These are financial obligations that you're expected to pay back. Understanding these is just as important as knowing your assets, because they directly subtract from your total wealth. It's a bit like balancing a scale, with assets on one side and liabilities on the other. A lot of people have these, so it’s pretty normal.

Mortgages: For homeowners, the mortgage is usually the largest liability. This is the loan taken out to buy property. Paying it down increases your equity, which in turn boosts your net worth, so it does.

Loans: This includes car loans, personal loans, student loans, and any other money borrowed from a bank or individual. These debts need to be repaid, often with interest, which is the way it goes.

Credit Card Debt: Balances carried on credit cards are a common liability. High-interest credit card debt can really eat into financial progress if not managed well, you know.

Other Debts: This could include medical bills, tax obligations, or any other outstanding financial commitments. Even small debts add up, so keeping track is helpful.

Common Ways People Build Wealth

When we think about how someone like "ugod" might accumulate wealth, it usually comes from a combination of different sources. Very few people become wealthy from just one income stream. It's often about diversifying where your money comes from and how it grows. This is a fairly typical pattern for wealth creation, it really is.

Earned Income

The most basic way to build wealth is through earned income. This is the money you get from working. For most people, it's their salary or wages from a job. For business owners, it's the profits their company generates. A high-paying job or a successful business can provide a strong foundation for saving and investing. This is, you know, the starting point for many.

Investments

Once income is earned, a significant path to building net worth is through investments. This means putting money into assets that have the potential to grow over time. Stocks can offer capital appreciation and dividends, while bonds provide regular interest payments. Real estate can appreciate in value and generate rental income. The key here is often patience and consistency. It's not a quick thing, usually.

Stock Market: Investing in publicly traded companies can lead to substantial gains over the long term. This is a very common approach, you see.

Real Estate: Owning property, whether it's your primary residence or rental units, can be a powerful wealth builder through appreciation and rental income. This is a tangible asset, which many people prefer.

Business Ownership: For many, starting and growing a successful business is the most direct route to significant wealth. The value of the company itself becomes a major asset, so it does.

Inheritance and Gifts

Sometimes, a person's net worth can get a substantial boost from an inheritance or large gifts. While this isn't something everyone experiences, it can certainly play a part in a person's financial standing. This is, you know, a fortunate circumstance for those who receive it.

Other Sources

Other sources might include royalties from creative works, proceeds from selling intellectual property, or even winnings from lotteries or contests. These are less common but can contribute significantly if they happen. It just goes to show, there are many paths to wealth, apparently.

Factors That Can Influence Net Worth

A person's net worth isn't static; it changes constantly due to various factors. When considering "ugod net worth," or anyone's wealth, it's important to look beyond just the current numbers and think about what makes them fluctuate. There are external forces, like the economy, and internal choices, like spending habits. It's a pretty complex interplay, you know.

Market Performance

The performance of financial markets has a huge impact, especially for those with significant investments. When the stock market is doing well, the value of investments tends to go up, boosting net worth. When markets decline, net worth can take a hit. This is, in a way, outside of individual control, but it's a big part of the picture.

Economic Conditions

Broader economic conditions, such as inflation, interest rates, and unemployment rates, also play a role. High inflation can erode the purchasing power of cash, while rising interest rates can make borrowing more expensive, affecting liabilities. A strong economy often means better job prospects and higher asset values, which is good for most people, naturally.

Personal Financial Decisions

Individual choices are arguably the most significant factor. How someone manages their income, how much they save, where they invest, and how they handle debt directly affect their net worth. Smart financial planning, disciplined saving, and wise investment choices can lead to substantial wealth growth over time. It's really about the choices you make, basically.

Saving Rate: How much of their income a person saves makes a huge difference. The more saved, the more can be invested, leading to greater wealth accumulation. It's a fundamental principle, actually.

Investment Strategy: The types of investments chosen and how they're managed also matter. A diversified portfolio often performs better and reduces risk over the long run. This is usually a key part of the strategy.

Debt Management: Keeping debt under control, especially high-interest debt, is crucial. Reducing liabilities directly increases net worth. It's a pretty straightforward connection, you see.

Spending Habits: Living within or below one's means frees up more money for saving and investing. Excessive spending, on the other hand, can hinder wealth building. It's about balance, in a way.

Life Events

Major life events can also influence net worth. Things like getting married, having children, buying a home, starting a business, or even facing unexpected medical expenses can all have significant financial implications, both positive and negative. These events, you know, reshape financial landscapes quite a bit.

How Net Worth is Often Estimated (Without Specific Data)

Since we don't have specific financial data for "ugod," discussing "ugod net worth" means looking at how such figures are generally estimated for public figures or entities when exact numbers aren't public. It's often a blend of educated guesses, public records, and industry averages. This is usually the case when precise details are not available, as a matter of fact.

Publicly Available Information

For known individuals, estimates often start with publicly available information. This might include reported salaries, known business ventures, real estate holdings (which are often public record), and major investments that are disclosed. For a hypothetical "ugod," if they were, say, a CEO of a publicly traded company, their compensation would be public. It's about piecing together what's out there, you know.

Industry Averages and Multiples

Analysts might use industry averages or revenue multiples to estimate the value of private businesses or assets. For example, if "ugod" was known to own a company in a specific sector, its value might be estimated based on typical valuations for similar companies. This is a common method when direct financial statements aren't accessible, you see.

Media Reports and Speculation

Often, net worth figures reported by the media are estimates, sometimes based on informed speculation. These are not always precise, as they rely on available clues and often don't account for private debts or less visible assets. It's important to take these figures with a grain of salt, frankly, as they are often just educated guesses.

Challenges in Estimation

Estimating net worth, especially without direct access to financial records, is incredibly challenging. Private debts are almost never public, and the true value of private business interests can be hard to determine. Market fluctuations also mean that even accurate estimates can become outdated very quickly. So, it's a bit of an art, not a precise science, you know.

Tips for Building Your Own Financial Strength

While we're discussing "ugod net worth" conceptually, the principles of building wealth apply to everyone. If you're looking to improve your own financial standing, there are several practical steps you can take. It's about making smart choices consistently over time. These are pretty common pieces of advice, actually.

1. Create a Budget and Stick to It

Understanding where your money goes is the first step. A budget helps you track your income and expenses, allowing you to identify areas where you can save. This gives you control over your money, which is very important. It's like a roadmap for your finances, you see.

2. Prioritize Saving and Investing

Make saving a regular habit, even if it's a small amount to start. Then, put those savings to work through investments. The earlier you start investing, the more time your money has to grow through the power of compounding. This is often called the "magic" of compounding, you know, because it really adds up over time.

3. Manage Debt Wisely

Focus on paying down high-interest debt first, like credit card balances. This frees up more money for saving and investing. Avoiding unnecessary debt also helps keep your liabilities low, which directly boosts your net worth. It's a pretty straightforward way to improve your financial picture.

4. Diversify Your Income Streams

While not always possible, having multiple sources of income can significantly accelerate wealth building. This could be a side hustle, rental income, or dividends from investments. It provides more financial stability, too, which is a good thing.

5. Continuously Learn and Adapt

Stay informed about personal finance and investment strategies. The financial landscape changes, so being adaptable and open to learning new approaches is valuable. There's always something new to learn, you know, about managing money. Learn more about personal finance on our site, and link to this page financial planning strategies.

6. Seek Professional Guidance

For complex financial situations, consider consulting with a financial advisor. They can offer personalized advice and help you create a robust financial plan. This can be a very helpful step for many people, really.

People Often Ask

Q: What's the difference between income and net worth?

A: Income is the money you earn over a specific period, like your monthly salary or annual business profits. Net worth, on the other hand, is a snapshot of your total financial value at a given moment, calculated by subtracting your total liabilities (what you owe) from your total assets (what you own). So, income is a flow, and net worth is a stock, you know, a cumulative figure.

Q: Can someone have a high income but a low net worth?

A: Absolutely. A person can earn a lot of money but if they also have very high spending habits, significant debt, or don't save or invest much, their net worth could remain low or even be negative. It's all about how income is managed and what choices are made with it, you see.

Q: How often should I calculate my net worth?

A: It's a good idea to calculate your net worth at least once a year, perhaps at the same time each year, to track your progress. Some people prefer to do it quarterly or even monthly if they're actively managing investments or paying down significant debt. Regular checks help you see how your financial health is changing, which is quite useful, actually. For more general information on financial health, you might find resources from the Investopedia helpful.

Understanding "ugod net worth," then, really boils down to grasping the general principles of financial health. It's about recognizing that wealth isn't just about how much money passes through your hands, but rather what you keep and what you own, after accounting for what you owe. Building a strong financial foundation, for anyone, involves a thoughtful approach to earning, saving, investing, and managing debt. It's a journey that takes time and consistent effort, but the rewards are well worth it, you know.

UGod Customs

UGod Customs

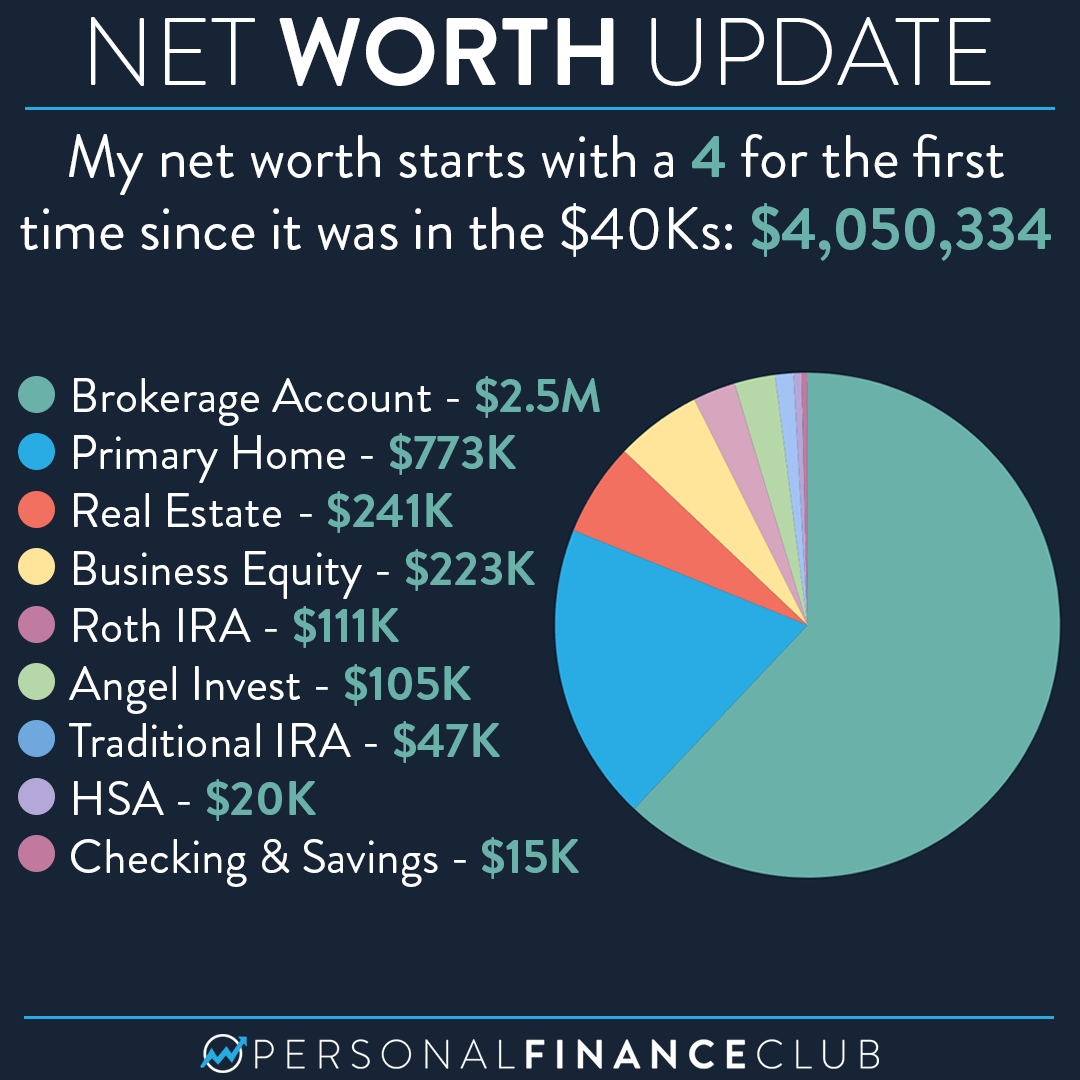

My $4 million net worth breakdown! – Personal Finance Club